Actions You May Want to Take Now as a Potential $2,000 Trump Payment Could Reach Americans Soon

The idea of a potential $2,000 payment to Americans has generated widespread attention across the United States. The proposal was discussed by President Donald Trump and quickly became a major topic in economic and political conversations.

Many Americans began asking the same question: could a payment like this really happen, and if so, when would the money actually arrive? At the moment, however, there is still significant uncertainty surrounding the proposal.

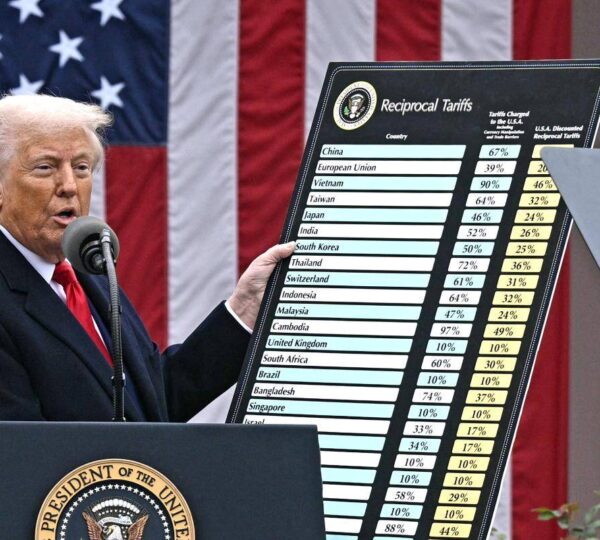

The concept behind the idea is what Trump described as a “tariff dividend.” In simple terms, it would involve using revenue collected from tariffs on imported goods and distributing part of that money back to American citizens.

Tariffs are taxes placed on goods imported from other countries. Governments sometimes use them to protect domestic industries, raise revenue, or encourage companies to produce more goods within the United States.

In recent years, tariffs have become a central part of the economic strategy promoted by the Trump administration. Supporters argue they help strengthen domestic manufacturing and reduce dependence on foreign production.

Critics, however, argue that tariffs can increase prices for consumers and create tension in international trade relationships. Because of this debate, the idea of redistributing tariff revenue to Americans has drawn both interest and skepticism.

In November 2025, Trump publicly suggested that Americans could receive a payment of at least $2,000 per person through this tariff dividend concept. The statement quickly circulated across news outlets and social media.

According to his remarks, the payments would likely exclude individuals with very high incomes. However, the exact income threshold that would determine eligibility has not yet been clearly defined.

The proposal also did not include detailed instructions explaining how the payments would be distributed or when they might arrive. This lack of specifics has contributed to the uncertainty surrounding the plan.

Although the proposal attracted attention, it is important to understand that no official law has been passed authorizing these payments. Without legislation, the federal government cannot distribute funds directly to Americans.

In the United States, federal spending decisions must generally be approved by Congress. This means lawmakers in both the House of Representatives and the Senate would likely need to approve any program that sends money to citizens.

Because of this requirement, experts say the proposal remains uncertain. Even if a plan is introduced, it would still need to move through the legislative process before becoming reality.

Economic analysts have also raised questions about whether tariff revenue alone would be sufficient to fund payments of this size. Independent estimates suggest the costs could be extremely large.

For example, some policy analysts estimate that providing $2,000 payments to millions of Americans could cost hundreds of billions of dollars depending on how eligibility rules are designed.

At the same time, federal tariff revenue, while significant, may not reach the level required to cover the full cost of such payments.

Recent government data suggests tariffs have generated tens or even hundreds of billions of dollars annually, depending on trade levels and policy decisions. However, the total revenue may still fall short of funding universal payments.

Because of these financial considerations, economists say the proposal would require careful planning if it were to move forward. Lawmakers would need to determine where additional funding might come from.

Some officials have also suggested that the proposed benefit might not necessarily arrive as a traditional cash check mailed to households. Instead, it could take other forms within the tax system.

One possibility mentioned in discussions is that financial relief could be delivered through tax reductions or deductions rather than a direct payment deposited into bank accounts.

For example, policies such as eliminating certain taxes or increasing deductions could reduce the overall tax burden for many households, which might function similarly to a financial payout.

These ideas have led to confusion among many Americans who initially expected a straightforward stimulus payment similar to those distributed during the COVID-19 pandemic.

During the pandemic, several rounds of stimulus checks were issued after Congress approved emergency relief packages. Those payments were authorized through legislation and funded through federal borrowing and spending programs.

The proposed tariff dividend, however, would operate differently because it would rely primarily on revenue generated from trade tariffs rather than emergency spending.

Another factor that may influence the proposal is ongoing legal debate surrounding the authority used to impose certain tariffs. Some tariff policies have been challenged in court.

If courts were to limit or overturn some of those tariffs, the expected revenue from them could change significantly. This would directly affect the amount of money available for any potential dividend program.

Because of these legal and financial uncertainties, policy experts advise Americans not to assume that a $2,000 payment is guaranteed. At this stage, the concept remains a proposal rather than an approved policy.

Still, the idea has sparked widespread discussion about how governments could potentially return revenue to citizens through dividends or rebates tied to economic policies.

Some countries and regions already use similar systems in limited forms. One example often mentioned is Alaska’s Permanent Fund dividend, which distributes a portion of oil revenue to residents each year.

That program demonstrates how governments can share revenue generated from natural resources or other sources. However, scaling a similar idea to the entire United States would involve far greater financial complexity.

Because of this complexity, lawmakers would likely need to negotiate details such as income limits, payment methods, eligibility criteria, and long-term funding mechanisms.

If such a program were ever approved, government agencies would also need to determine how payments would be distributed to eligible recipients.

In many cases, the Internal Revenue Service plays a central role in administering large-scale payments to households, particularly when tax records are used to verify eligibility.

For that reason, financial experts recommend that Americans keep their tax information accurate and up to date, even when potential programs remain uncertain.

Maintaining accurate tax filings ensures that individuals can receive government benefits quickly if a program is approved in the future.

Financial planners also encourage households to think carefully about how they might use unexpected money if it becomes available.

Unexpected funds can provide an opportunity to strengthen personal finances, reduce debt, or increase long-term savings.

One commonly recommended strategy is placing extra money in a savings account that earns interest over time.

High-yield savings accounts and money market accounts currently offer interest rates that are higher than traditional savings accounts offered by many banks.

While interest rates change over time, some savings products have offered returns around four percent annually in recent years.

For example, if someone placed $2,000 into an account earning four percent interest, the money could generate roughly $80 in interest over a year.

Although this amount may seem modest, the benefit increases if the account holder continues adding money regularly.

If a person adds an additional $100 each month while earning interest, the balance could grow much faster over time.

Savings accounts can also provide a financial safety net in case of emergencies such as unexpected medical expenses, car repairs, or temporary loss of income.

Another common recommendation from financial advisors is using extra money to pay down high-interest debt.

Credit card balances, for example, often carry interest rates far higher than most savings accounts can earn.

Reducing debt can therefore provide long-term financial benefits by lowering future interest payments.

Some households might also choose to invest extra funds in retirement accounts or other long-term investment strategies.

However, investment decisions depend on individual financial situations, risk tolerance, and long-term goals.

Because every household’s financial situation is different, experts emphasize that there is no single correct way to use unexpected money.

Budgeting, saving, and investing decisions should always reflect personal circumstances and financial priorities.

For now, though, the most important point remains that the proposed $2,000 payment has not been approved by Congress.

Without legislative approval, the federal government cannot move forward with distributing funds to citizens on a nationwide scale.

Political proposals often generate headlines and public discussion long before any official policy is implemented.

In many cases, ideas change significantly during the legislative process as lawmakers negotiate details and funding options.

Sometimes proposals are modified, delayed, or ultimately rejected depending on political priorities and budget constraints.

Because of this, experts encourage Americans to rely on official announcements from government agencies rather than social media speculation.

Accurate information typically comes from official statements, congressional legislation, and announcements from federal agencies responsible for administering programs.

Until those steps occur, any timeline for payments remains uncertain.

That means Americans should remain cautious when reading headlines suggesting that payments are guaranteed or arriving soon.

While the proposal has sparked interest and debate, the final outcome will depend on decisions made by lawmakers and economic policymakers.

In the meantime, individuals can take practical steps to prepare for potential financial opportunities or challenges.

Keeping tax records organized, maintaining savings, and staying informed about policy changes can help households remain financially resilient.

Economic proposals often evolve over time, and future versions of the idea could differ significantly from the original announcement.

If a policy is eventually approved, government agencies would likely provide clear guidance explaining eligibility requirements and payment procedures.

Until then, the proposed tariff dividend remains an idea under discussion rather than a confirmed government payment.

For millions of Americans, the possibility of additional financial support is certainly appealing, especially during times of economic uncertainty.

However, responsible financial planning should never depend entirely on money that has not yet been officially authorized.

Staying informed, maintaining realistic expectations, and managing finances carefully are the best strategies while policymakers continue debating potential economic initiatives.

Whether the $2,000 dividend proposal ultimately becomes reality or not, the conversation surrounding it highlights the broader discussion about economic policy, taxation, and how government revenue might be used in the future.

{kind=link}